Telemedicine and Telecoms – A new treasure trove or Pandora’s box of data

.png.aspx?lang=en-GB)

Telemedicine presents new business opportunities to telecoms. However, the space can also lead to increased risk exposure. One area where telecoms must be particularly observant is handling and processing patient data.

Across industries, COVID-19 has brought changes, also for telecoms. Industry walls are increasingly fluid, opening new opportunities. One example is telecoms’ potential for growing their market presence in telemedicine.

The pandemic has increased customer demand for contactless diagnosis, voice/video healthcare services, online primary care, and more – all heavily reliant on telecoms’ communication infrastructure. Furthermore, telecoms are excellently positioned to develop and implement healthcare technology solutions – either alone or in partnership with other companies.

Telemedicine remains an incipient market – albeit one garnering intense interest. More than 170 start-ups and scale-ups working on new solutions raised more than US$10 billion in 2020, almost double that of any previous year. However, the amount pales in comparison to the potential market for disruptive solutions. In most developed countries, more than 10% of GDP goes to healthcare. Estimates put the worth of the global health industry at US$8.45 trillion in 2018, and global healthcare spend growing to $10 trillion by next year.

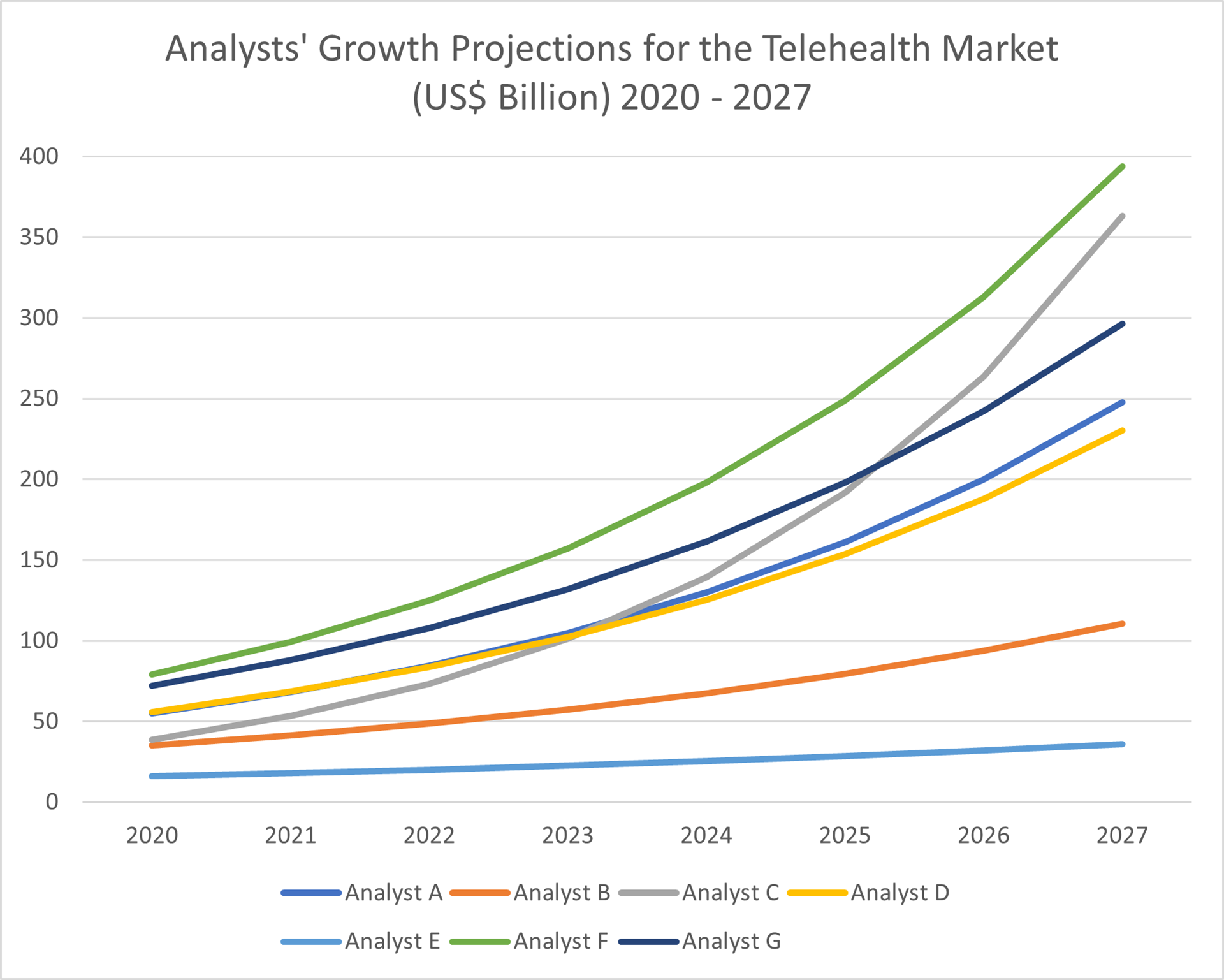

Data, graph: BDO Global – Based on market forecasts and predicted CAGR rates from selected, anonymised market analysts.

Proprietary BDO Global analysis of market forecasts shows telemedicine set to grow at a compound annual growth rate of around 23% to a market size of approximately US$200 billion by the middle of the decade.

Telecoms companies are excellently positioned to take advantage of the changes and growing market. However, risks linked to dealing with and processing sensitive patient data is one of several areas which must be carefully addressed if telemedicine ventures are to become successful for telecoms.

Growing Telehealth Market Opportunities

2020 and 2021 have seen rapid changes to customer preferences across industries. Simultaneously, existing trends have accelerated as mobile and home-delivered services prosper. This also applies to the healthcare space.

Telemedicine overlaps somewhat with telehealth but spans a broader array of solutions and service delivery systems. Video consultations, patient record handling, remote monitoring, and wearable healthcare devices are just the tip of the iceberg. Faster, more affordable care delivery for patients and reduced solution costs and new revenue streams for providers are just a couple of advantages leading to the space set for rapid growth.

A short (very non-exhaustive) list of select telemedicine solutions and services includes:

- Online primary care

- Online consultations

- Wearable health monitoring

- Remote patient and healthcare staff training

- Message reminders of upcoming exams or preventive care

- Transfer of medical data (records, pictures, videos)

- Online prescription handling

- Web-based communication with out-patients

- Vital sign monitoring

- Online appointment scheduling

Abundant Telecoms Opportunities

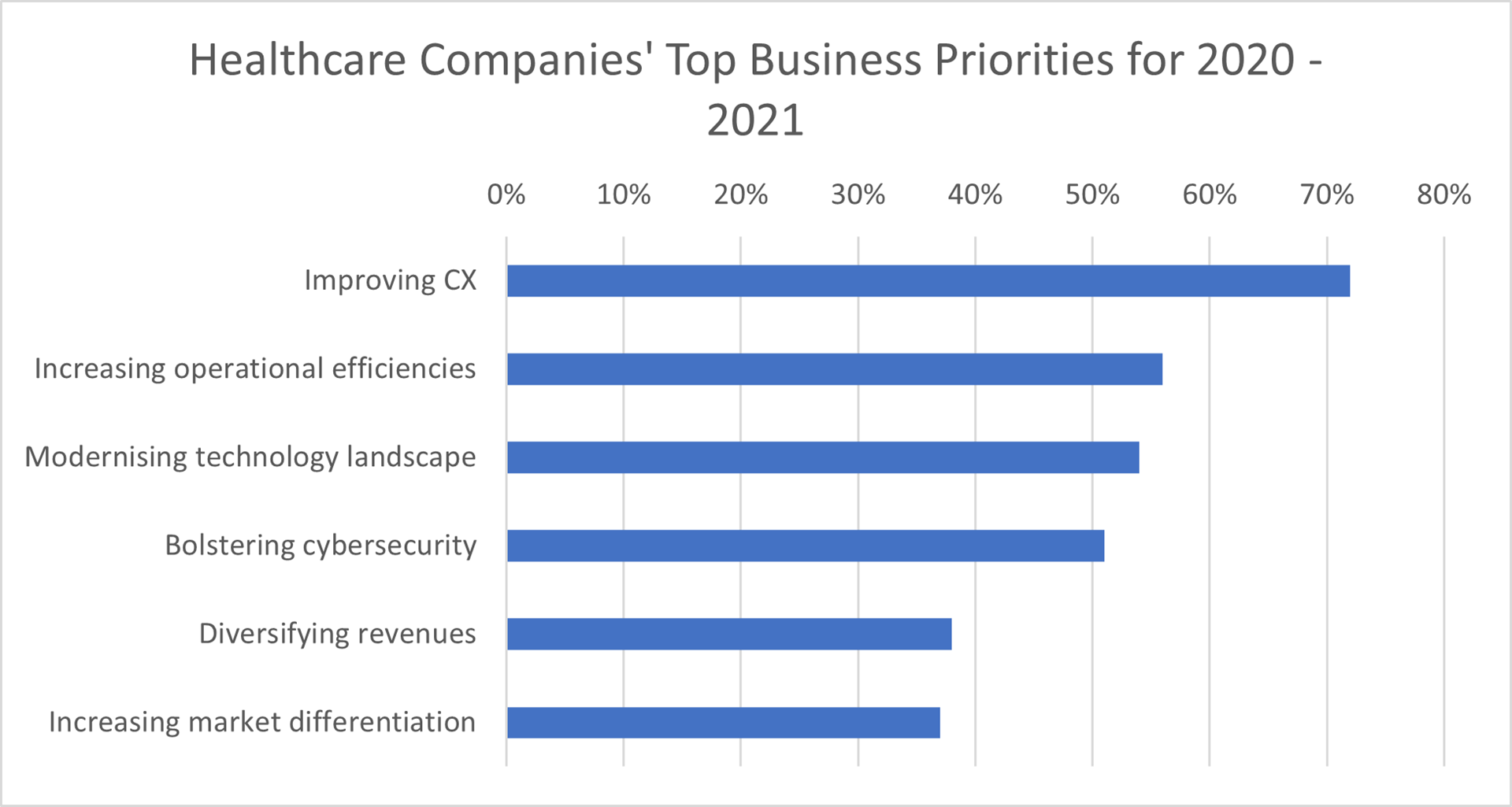

The list above represents just some areas where telecoms companies could build out a presence either alone or through partnerships. BDO’s 2021 Healthcare CFO Survey highlights that healthcare companies are increasingly open to pursuing the latter as the industry increases digitisation and works on improving customer experience (CX).

Data: BDO 2020 Healthcare Digital Transformation Survey, Graph: BDO Global

Some of the areas and strategies that may be worth considering include:

- Consumer wellness and self-care: Includes consumer-facing applications and devices. User goals include general fitness and health monitoring. Smaller telecoms with a national or regional strong position and expertise with data handling may look to build out a healthcare presence by partnering with global health-tech players, such as healthcare Vertical Software-as-a-Service companies.

- Remote care delivery & monitoring: Focused on hardware and software solutions provided to healthcare staff and patients, including online appointment bookings, web-based health monitoring, prescription management, and video consultations. Telecoms can often find advantages by partnering with healthcare companies or make acquisitions in the space to deliver end-to-end services.

- Insurance and administrative solutions: Focusing on IT systems that assist hospitals, GPs, labs, and insurance companies manage patient records and day to day activities. Solutions are often subject to local rules and regulations, so most providers tend to be locally based or partner with local companies. A strong area for telecoms looking to build out solutions or expand through partnerships or M&A.

- AI- and data analytics-based healthcare: Advanced analytics and AI analysis to improve nearly all aspects of healthcare delivery. Builds on data and connectivity, and access to and processing of, making this opportunity more accessible to telecoms that have expertise in managing various types of data for multinational-level enterprises.

Examples of Telecoms Pursuing Telemedicine

Telecoms considering the telemedicine space can look to a growing list of real-world examples for inspiration.

One example comes from Spain, where Telefónica has rolled out an e-health service through its domestic retail unit, Movistar. Movistar partnered with telemedicine provider Teladoc Health and launched a healthcare service that provides customers with around-the-clock access to primary care doctors for €6.95 per month (€10.95 for a family of two adults and two children). The service includes remote video or phone consultation, which doctors use to diagnose, prescribe medicine, or refer patients. It also has a digital symptom pre-assessment that uses AI to cross-reference people’s complaints and compare them with more than 600 common diseases and injuries, using it to offer automated advice on possible next steps.

In the US, AT&T offers healthcare providers solutions including patient check-in, in-facility navigation, online healthcare services, and patient monitoring. Its approach often involves partnering with start-ups. One example is its partnership with patient engagement specialists Gozio Health on indoor wayfinding and waiting time monitoring in healthcare settings (for example, hospitals). Another is its partnership with MobileSmith Health, which provides pre-op and post-op advice and adherence monitoring for patients to reduce hospital costs and improve patient outcomes.

In the UK, BT has gradually been expanding its healthcare-related endeavours. One example is its contract to digitise around 50 million patient records, while another is its involvement in a project to perform remote diagnostics procedures via 5G. The latter happened in collaboration with University Hospitals Birmingham NHS Foundation Trust (UHB).

Other avenues are also on the event horizon, with ABI Research predicting AR and VR-based health services to generate revenues around $10 billion and $1.2 billion respectively by 2024. Furthermore, IDC predicts that almost half of hospital technology spending by 2023 will go to cloud, mobility and IoT.

Data Risks Abound

All the services mentioned above are heavily reliant on robust and secure connectivity, a core competence of telecoms. Telecoms are also used to dealing with data, and data-related risks are already top-of-mind for telecoms. This fact was highlighted in BDO’s recent Telecoms Risk Factor Survey, where telecoms pointed to several data-related risks as among the most pressing they face.

One reason is the emergence of new legislation appearing across the world to regulate and secure the transfer, processing and use of customer data; something particularly pertinent in the healthcare space.

Finding ways to handle data and data transfer safely and securely will be part of any venture in the telemedicine space for telecoms companies. It does also represent an area where companies may be able to deliver stand-alone solutions.

Other risk factors which need to be addressed by telecoms include healthcare delivery and patient data compliance issues. Furthermore, the (until recently, at least) relatively slow pace of technological change in the healthcare space is also a factor.

From a systems perspective, other factors include system variations, including in maturity levels, which can affect the ability to implement, integrate and scale new technologies.

Finding Ways to Mitigate Risks

For telecoms, mitigating the risks associated with endeavours in the healthcare field includes technical and social aspects, as well as communication efforts.

For the hardware and technical side, all efforts should be taken to mitigate the risk of hacks or loss of data.

Some of the measures to consider include:

- Implementing exhaustive monitoring covering all in- and outgoing traffic and network elements

- Extensive use of firewalls and user validation rule – sacrificing speed for security can be a good choice.

- Perform regular assessments and tests of network security.

- Consider real-time (perhaps AI-powered) anomaly detection systems.

Social and company culture aspects will invariably play a large role in how data is treated. This is doubly true in situations where several companies are involved in the project. Telecoms should be working closely with all involved parties to evolve clear IT security policy rules and regulations.

Furthermore, it may be useful to consider crises communication strategies and how to divulge a potential hack to the relevant organisations and society in general.

Similar multi-tiered risk mitigation strategies should be evolved and deployed across all areas.